The Prove-It Cloud and the Long-Run AGI Crowd

Does the public market believe in AGI?

The investment in AI is valued on obtaining AGI, yet it’s important to distinguish that the market is valuing the AI spenders remarkably different than they are valuing the AI model layer. While it is reasonable to assume that the growth-oriented AI model layer should trade at a premium due to having unencumbered corporate structures compared to the steady growth large-cap financiers where AI is one line in an already busy balance sheet; the actual difference shows a public market expecting reasonable return from AI infrastructure with the private market expecting frankly ‘insane’ returns from AGI. Many mark this up to the private market having the leeway of a much longer 10-15 year time horizon, while the public markets have shared memory of boom-and-bust cycles related to technology. The question for the public markets in the coming month and year is whether they will extend the pessimistic public market reading to the AI modelers, or will the euphoria of the private market bleed over?

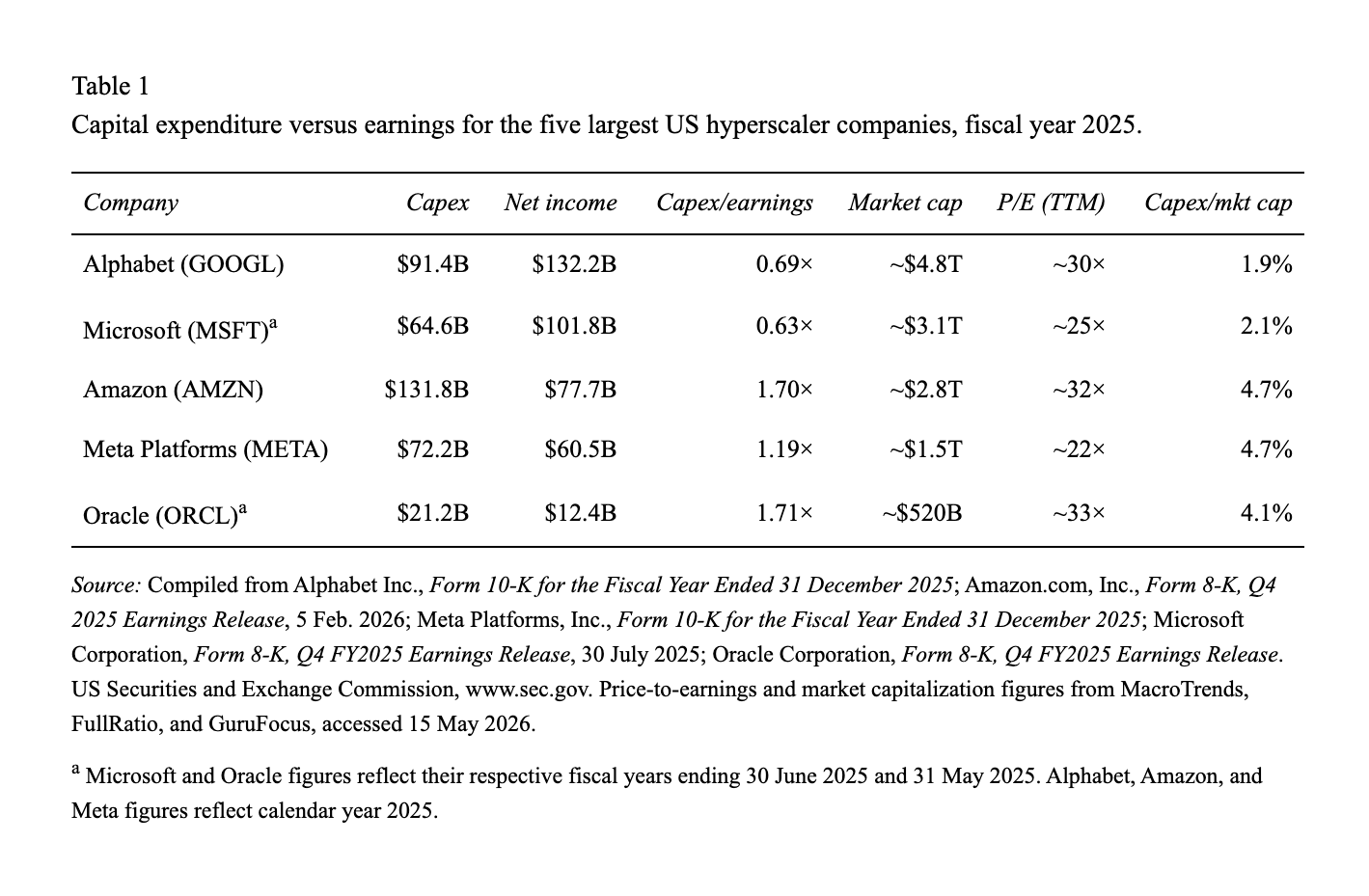

According to Epoch AI the capital expenditures [capex] for new growth across the major AI cloud infrastructure players [Alphabet, Amazon, Microsoft, Meta, and Oracle] increased an average of 72% yearly since 2023, with $770 billion projected in 2026 (Epoch AI, 2026). The ratio of capex to earnings is noticeable with Amazon, Meta, and Oracle spending more than their yearly income on build out (Table 1). While these companies have a high expectation for the continued growth of AI, the contrarian datapoint is that they had an average 12-month trailing P/E through May 2026 of 32x, which is in-line with the S&P500 historical 10- year average of 28x. The biggest spenders on AI are not being priced by the market like internet stocks were during the dot-com bubble. The prices are, very reasonable, considering some stocks such as Cisco saw numbers as high as 200x in its heyday. In other words, the market is basically forcing the AI spenders to prove their expense, even though their spending is associated with tangible assets that will remain even without AGI.

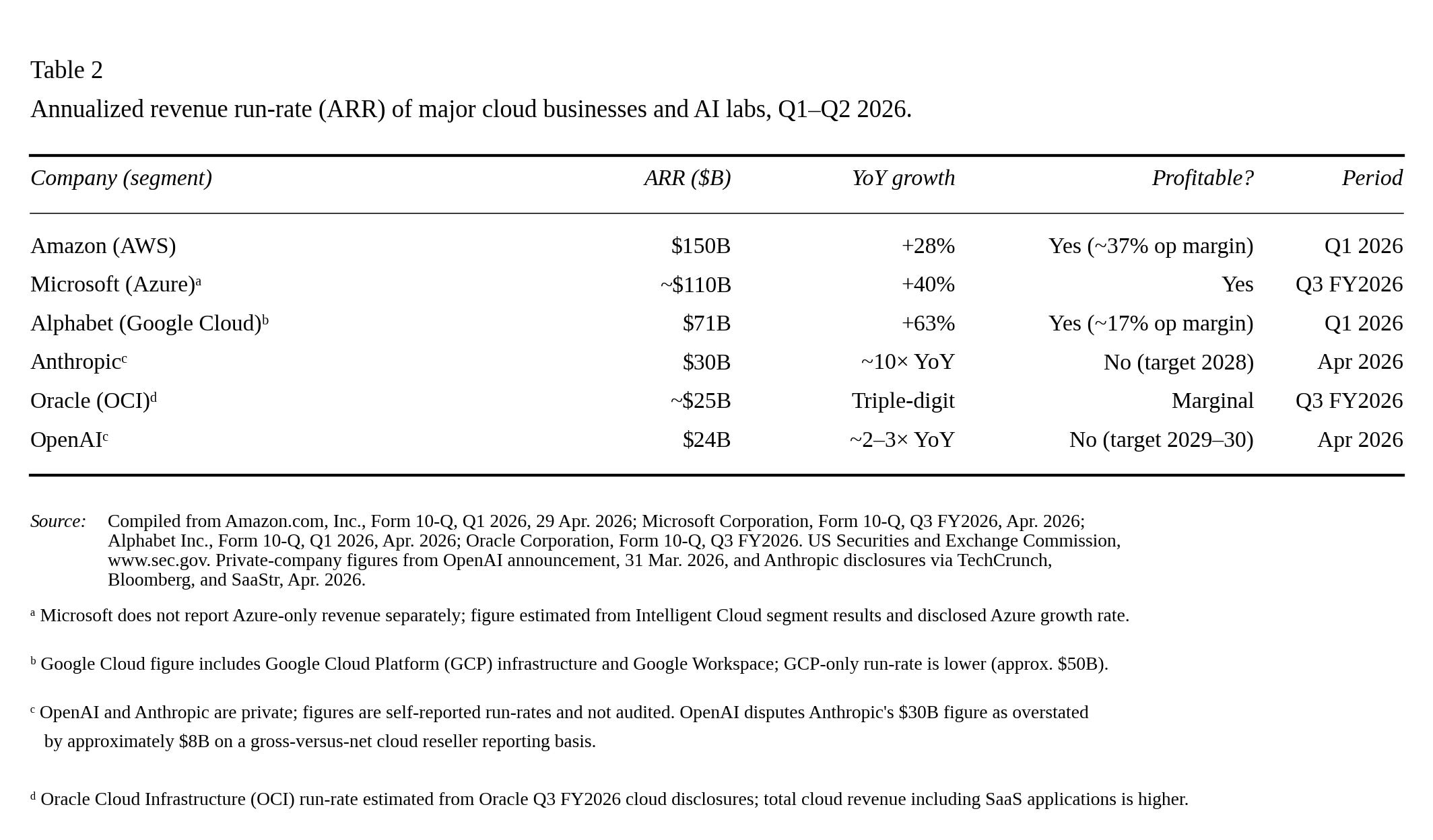

On the other hand, the AI application level is almost entirely private with a March 2026 private equity raise by OpenAI at $122 billion, valuing the company at $852 billion (OpenAI Press Release, 2026). Anthropic is the more surprising valuation having quickly grown from $380 billion valuation based on February 2026 raises to valuation of $900 billion bases on deals in works as of May 2026 (Bloomberg, 2026). The reason for these valuations are based on OpenAI’s $24 billion annual revenue and Anthropic’s 30B annual revenue [or $22 billion if you agree with OpenAI’s argument that Anthropic misreported their number (Remio, April 2026)].

Now let’s consider these in comparison (See Table 2). The implied growth rate of Anthropic is out of this world at 10x and OpenAI at 2-3x! Oracle is a core outlier from the other cloud names but that is specifically due to the cyclical nature of their OpenAI relationship with $600 billion in new cloud infrastructure build out to support them. There are some great articles out there discussing the cyclical nature of these relationships, so I’ll skip discussion here (Breckinridge, April 2026; MUFG, December 2025). The point I’m wanting to note is that the AGI race is being played out entirely outside of the infrastructure AI spending realm, even with the cyclical nature of the relationships. While the public market only has access to this one layer, it reflects an important caveat when the model companies start to IPO.